Master Cash Flow: Track, Plan, and Grow What You Keep

Master cash flow by tracking every dollar, planning bills and buffers, fixing leaks, and investing surplus so your money grows, and you keep more.

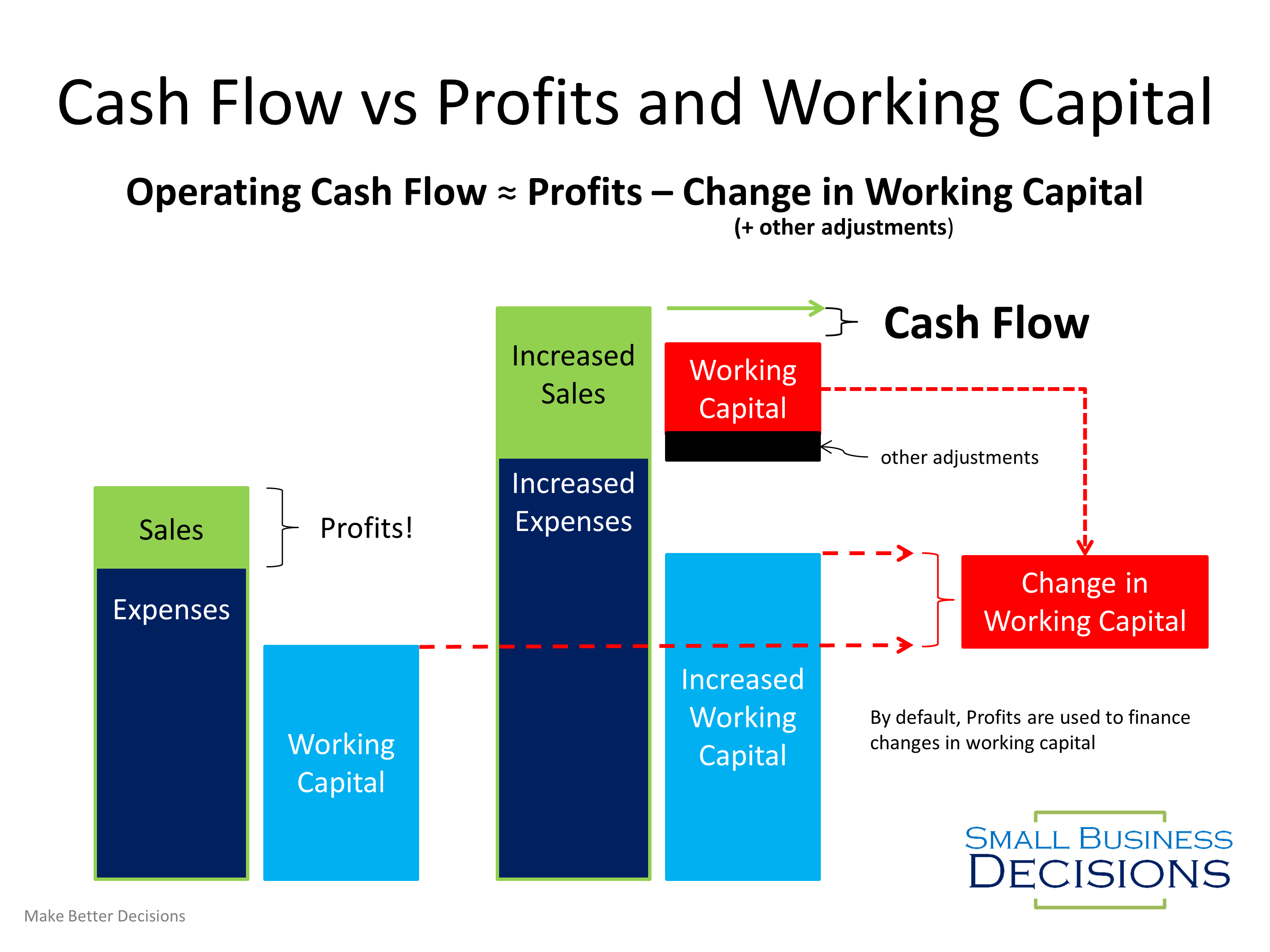

Cash Flow, Not Just Income

Mastering cash flow is about what stays in your pocket after money moves in and out. Many people chase higher income, but without control of outflows, lifestyle creep consumes gains. Cash flow is the household oxygen: it determines options, reduces stress, and funds goals on your timeline. Start by defining the equation clearly: net cash flow equals total inflows minus total outflows across a chosen period. Inflows include paychecks, benefits, refunds, small side income, and irregular windfalls. Outflows include bills, living costs, debt payments, transfers to savings, and those forgettable micro purchases that quietly add up. Healthy cash flow is consistent, predictable, and resilient to small surprises. The goal is not perfection; it is to increase the gap between what arrives and what departs, then channel the surplus to priorities you pick in advance. When you master timing, patterns, and decisions, you turn money from a source of uncertainty into a reliable engine for freedom, stability, and growth.

Track Every Dollar

You cannot improve what you do not measure, so start with complete tracking. Pull statements from every account where money moves: checking, savings, credit cards, and cash withdrawals. Aggregate them in a simple spreadsheet or a trusted app, then reconcile weekly so your picture stays fresh. Tag each transaction with a clear, minimal set of categories to avoid analysis paralysis. Think housing, utilities, transit, groceries, dining, health, insurance, debt, savings, giving, and fun. Add a note to unusual charges, and split transactions when a single purchase covers multiple categories. Do not ignore cash; create a small cash category and log withdrawals as expenses to keep them visible. After a few cycles, calculate average inflows, average outflows, and net cash flow for each month. Look for patterns like high spending at the end of pay periods or spikes around social events. Clarity here reveals quick wins and builds the momentum you need for lasting changes.

Categorize With Purpose

Categories are levers. Sort spending into fixed and variable, then label items committed versus flexible to highlight where choices exist. Fixed costs include rent, baseline utilities, insurance, and minimum debt payments. Variable costs include groceries, dining, fuel, discretionary shopping, and entertainment. Committed items are those you cannot change quickly; flexible items offer room for tradeoffs. Treat pay yourself first transfers to savings, investments, sinking funds, or debt prepayments as nonnegotiable expenses that happen near payday. This reframes savings from what is left over into something deliberate. For clarity, group categories by goals: living essentials, safety and health, mobility, learning, joy, and future you. Aim for a small number of buckets so you can actually manage them. Add a miscellaneous buffer to catch oddities and reduce budget friction. The outcome is a spending map that tells you which dials to turn when cash gets tight and which habits to reinforce when cash is abundant.

Map the Money Calendar

Cash flow is not just how much, it is also when. Sketch a monthly money calendar that shows paydays, bill due dates, recurring subscriptions, and typical spending spikes. If paychecks land midweek while major bills draft early in the month, you might experience short, stressful squeezes even when the averages look fine. Solve this with a buffer that covers at least one week of expenses, then grow it until you comfortably align due dates after income hits. Consider a simple account architecture: an Income Hub that receives all inflows, a Bills account for fixed payments, a Spending account for day to day purchases, and a Savings account for goals and reserves. Automate transfers from the hub on payday so the right amounts flow to each destination. This design creates guardrails, reduces overdraft risk, and makes it obvious when a category is running hot. Your calendar becomes a control panel for predictable, calm money management.

Design a Practical Budget

A budget is a plan for your cash to follow, not a cage. Choose a framework that fits your style. A zero based budget assigns a job to every dollar so nothing sits idle. A simple percentage plan sets targets for needs, wants, and savings. An envelope or category method caps variable spending and rolls any leftover to the next period. Whatever you pick, include sinking funds for non monthly costs like car maintenance, medical deductibles, travel, gifts, and home repairs. Fund them on payday so big expenses arrive as mild inconveniences, not emergencies. Keep variable categories realistic; if groceries always exceed your target, adjust the target or change the behavior, but do not pretend. Use automation to move money on schedule and relieve decision fatigue, then add friction where you overspend by separating fun money from essentials. The best budget is the one you can live with consistently, not the most complex.

Turn Surplus Into Growth

Once you create a gap, direct that surplus with intention. First, secure stability: build an emergency fund that covers a few months of essentials and park it where you will not accidentally spend it. Next, accelerate debt payoff using the avalanche method for interest efficiency or the snowball method for motivational wins. Simultaneously, cut recurring costs you no longer value. Negotiate internet and phone bills, trim unused subscriptions, optimize insurance deductibles, and improve home energy habits. On the income side, look for quick lifts: ask for a raise with evidence, refine a side hustle, sell idle items, or upskill to unlock higher rates. Automate savings to long term accounts so growth compounds quietly. Revisit withholding and estimated payments to avoid large surprises while staying compliant. Document every play you try and the result it produced. The goal is simple: transform extra cash into durable capacity that continues paying you back.

Forecast, Stress Test, and Protect

Build a forward view so you can steer, not react. Start with a rolling cash forecast that projects inflows, bills, variable spending, and transfers for the next few months. Use conservative assumptions and add a line for one off items you can already see coming. From that forecast, calculate a safe to spend number for the week, then check it during your routine. Stress test your plan with what if scenarios: a small income drop, a medical bill, a car repair, or a temporary move. Identify the steps you would take in each scenario now, not later. Strengthen your emergency fund, keep adequate insurance for health, liability, home, and vehicles, and secure documents with backups. Freeze credit where appropriate and monitor statements to catch fraud early. A clear forecast paired with protection creates confidence. You are not predicting the future; you are preparing your cash to adapt without derailing your goals.

Routines That Compound

Consistency turns a plan into progress. Set a weekly money date to reconcile transactions, check category balances, and make one tiny improvement. Run a monthly close where you review the budget versus actuals, move any leftover to priorities, and reset envelopes. Do a quarterly reset to adjust targets, rebalance subscriptions, and update sinking funds for upcoming events. Track simple metrics: savings rate, net cash flow, debt to income, and months of runway covered by reserves. Celebrate wins like a fully funded category or a negotiated bill reduction, and document a lesson learned when you miss. Keep your system light enough that you will keep using it, eliminating steps that add complexity without insight. Over time, your habits become structural advantages. The result is a life where money supports what matters, surprises are manageable, and you grow what you keep with calm, repeatable decisions.